How to apply

Target Groups and Application Eligibility:

Proprietors who disagree with the result of the immovable property evaluation.

Application Approach:

- In person at the counter: application should be made by the applicant in person, or by an authorized person;

- Mobile application “Macau Tax”;

- FSB Electronic Services.

Required Document:

- Urban Property Tax – M/6 – “Application for Special Evaluation”;

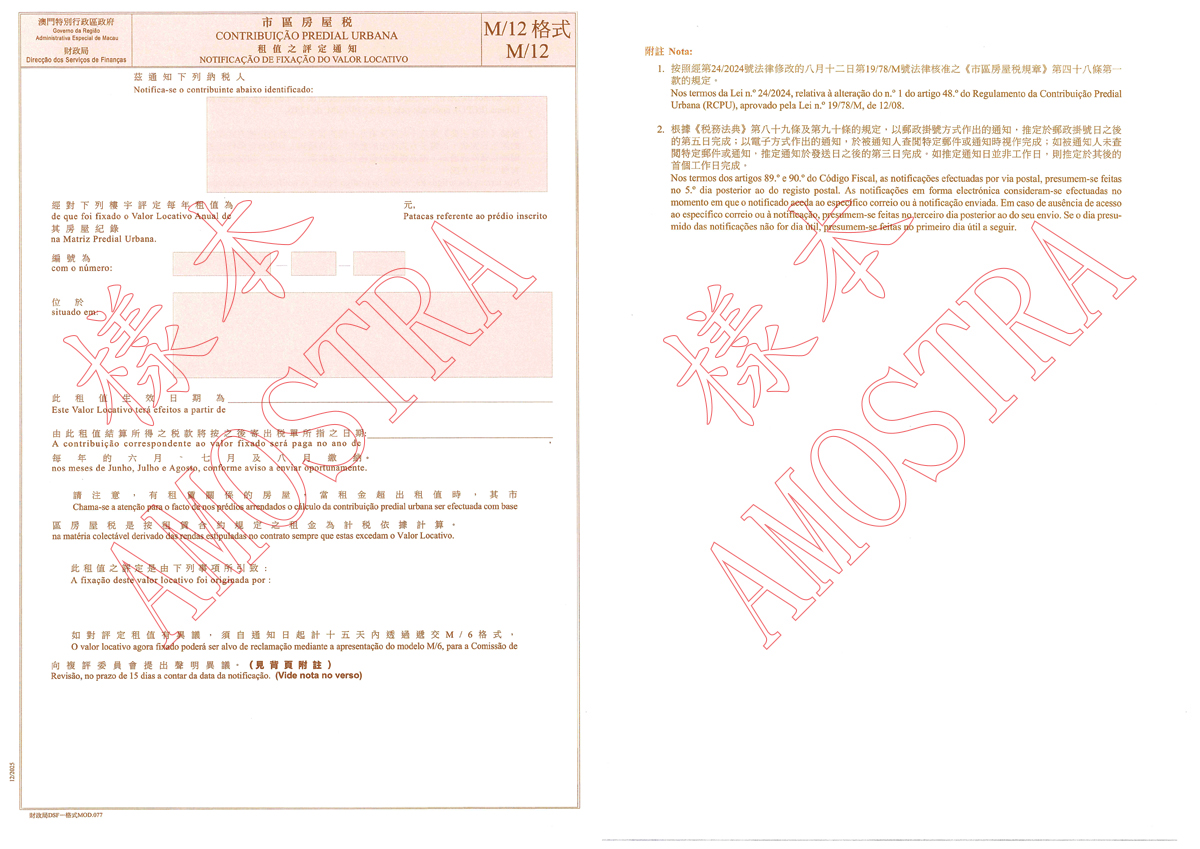

- A copy of Property Tax – M/12– “Notification of Rental Value Evaluation” and the related envelope;

- Copy of the proprietor’s identity document, if the proprietor is a legal entity, a copy of the Commercial Registration Certificate issued by the Commerce and Movable Property Registry is required;

- Copy of the witness’s (who is appointed by the applicant) identity document.

{kind=link}

Document must be presented:

- The applicant (individual, or legal representative of the company or the association) shall present the original of his/her identity document, or the relevant certification documents of company or association representative (if the business registration has been completed and this Bureau can check the relevant information through the Legal Affairs Bureau’s online inquiry system, there is no need to submit a business registration certificate);

- The agent handling the application shall present the original of applicant’s identity document or a power of attorney;

- The applicant who holds identity document without signature shall apply in person.

Time Needed:

An objection must be lodged with the Review Committee within 15 days from the notification date of the Urban Property Tax – M/12 – “Notification of Rental Value Evaluation”.

Service location and office hours

Application Location:

- The“Finanças” Building – Tax Services Centre:

Ground floor, the “Finanças” Building, 575, 579 & 585 Avenida da Praia Grande, Macao. - Macao Government Services Centre – Taxation:

Ground floor, 222 Avenida de Venceslau de Morais, Macao. - Macao Government Services Centre in Islands – Taxation:

Third floor, 225 Rua de Coimbra, Taipa.

Office Hours:

Monday to Friday: 09:00 – 18:00

Closed on weekends and public holidays

Remark / Guidance notes

Remarks:

- The lessor, lessee, or sublessee is responsible for facilitating the Review Committee’s work and providing any necessary explanations related to the valuation;

- According to Article 89 of the Fiscal Code, notifications sent by registered mail are presumed effective on the fifth day after the date of mailing. Article 90 of the Fiscal Code states that notifications made electronically are deemed effective when the addressee accesses the specific message or notice sent to the electronic address declared under paragraph 3 of Article 21 of the Fiscal Code. If the addressee does not access the message or notice, the notification is presumed effective on the third day after the date of dispatch. If the presumed date of notification is not a business day, it is instead presumed effective on the next business day;

- If the rental value determined by the Review Committee exceeds the value proposed by the appellant or in the application by more than 25%, the taxpayer shall be liable to pay a tax equivalent to 3% of the new taxable basis for each assessment, to compensate for the expenses incurred;

Taxation

Tax