How to apply

Target Groups and Application Eligibility:

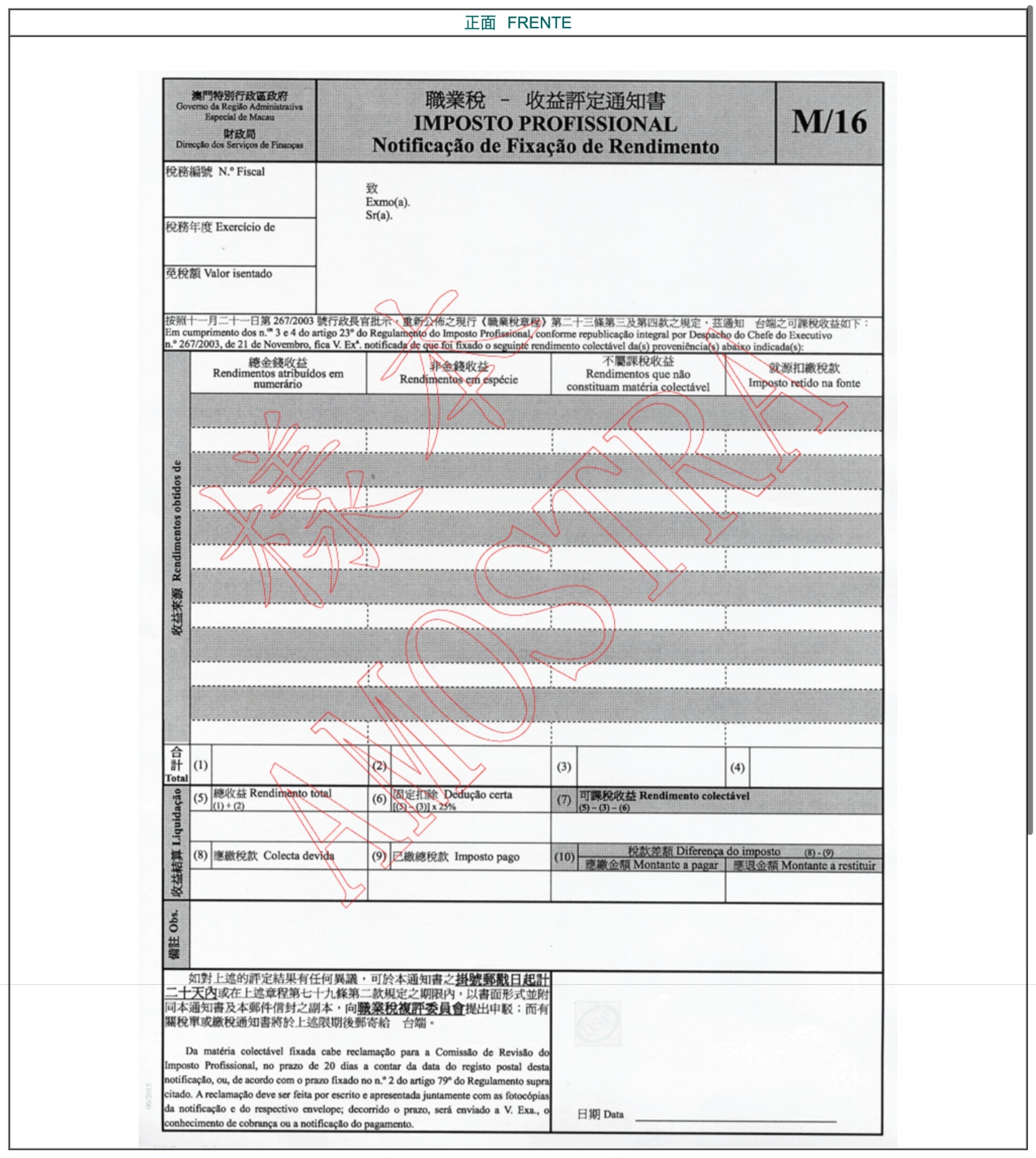

Salaries Tax taxpayers who disagree with the assessment of taxable income.

Application Approach:

Application should be made by the applicant in person, or by an authorized person.

Required Document:

- Objection must be lodged in writing and sent to the Chairperson of the Re-evaluation Committee, as well as supporting documents that the taxpayer may regard as necessary;

- A copy of the Salaries Tax-M/16-“Notification of Income Assessment” and the relevant envelope.

{kind=link}

Document must be presented:

- The applicant shall present the original of his/her identity document;

- The agent handling the application shall present the original of applicant’s identity document or a power of attorney;

- The applicant who holds identity document without signature shall apply in person.

Time Needed:

Within 15 days upon a receipt of the Salaries Tax-M/16-“Notification of Income Assessment”.

Service location and office hours

Application Location:

- The“Finanças” Building-Document Receiving Desk:

First floor, the “Finanças” Building, 575, 579 & 585 Avenida da Praia Grande, Macao. - Macao Government Services Centre-Taxation:

Ground floor, 222 Avenida de Venceslau de Morais, Macao. - Macao Government Services Centre in Islands-Taxation:

Third floor, 225 Rua de Coimbra, Taipa.

Office Hours:

Monday to Friday: 09:00-18:00

Closed on weekends and public holidays

Remark / Guidance notes

- The 5th day commencing the postmark date of the registered notice will be considered as the day taxpayer gets informed. If the 5th day is a non-working day, the subsequent next working day will be substituted. Saturdays are regarded as working days for postal service;

- An objection lodged against the assessment of taxable income has the effect of holdover of payment of tax until the Re-evaluation Committee has made its determination;

- The Re-evaluation Committee will review the taxable amount and re-evaluate when the objection is entirely or partially resolved;

- The taxpayer will receive a written determination made by the Re-evaluation Committee;

- A judicial appeal against the determination made by the Re-evaluation Committee must be lodged within 45 days.

Taxation

Tax